Source: AFP.

Rising gold prices has been one of the strongest trends so far this year. The gold rally stalled earlier but resumed over the past week with gold making a new record high. Stronger prospects of the Federal Reserve (Fed) easing, concerns about both the Fed’s independence and the safety of fiat money have revived buying interest in gold. We remain bullish gold and have a 12-month target of USD3,900/oz. Concerns over the Fed’s independence are present in asset prices but remain muted. Gold can easily overshoot USD4,000/oz if these concerns escalate.

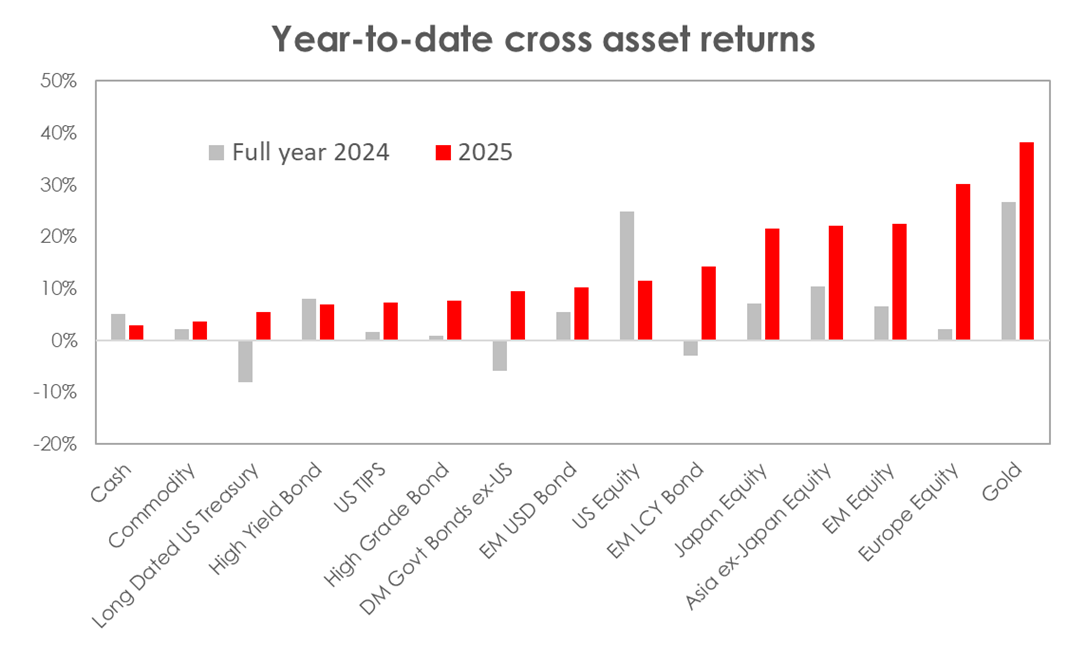

Gold has been one of the strongest trends so far in 2025

Source: Bloomberg, Bank of Singapore

Gold is a non-yielding asset, unlike equities, which pay dividends and bonds, which pay interest. Gold prices tend to increase when the Fed eases because the opportunity cost of holding gold falls when US interest rates decline. Tariff uncertainty has kept the Fed on hold this year after cutting by 100bp to 4.25%-4.50% in the second half of 2025. However, softer US labour market data has increased the likelihood of the Fed resuming rate cuts in September. We now expect the Fed to cut 25bp at each of the three remaining FOMC meetings in 2025. As the Fed eases, the USD is likely to depreciate. This should catalyse further gold ETF inflows and push up gold prices.

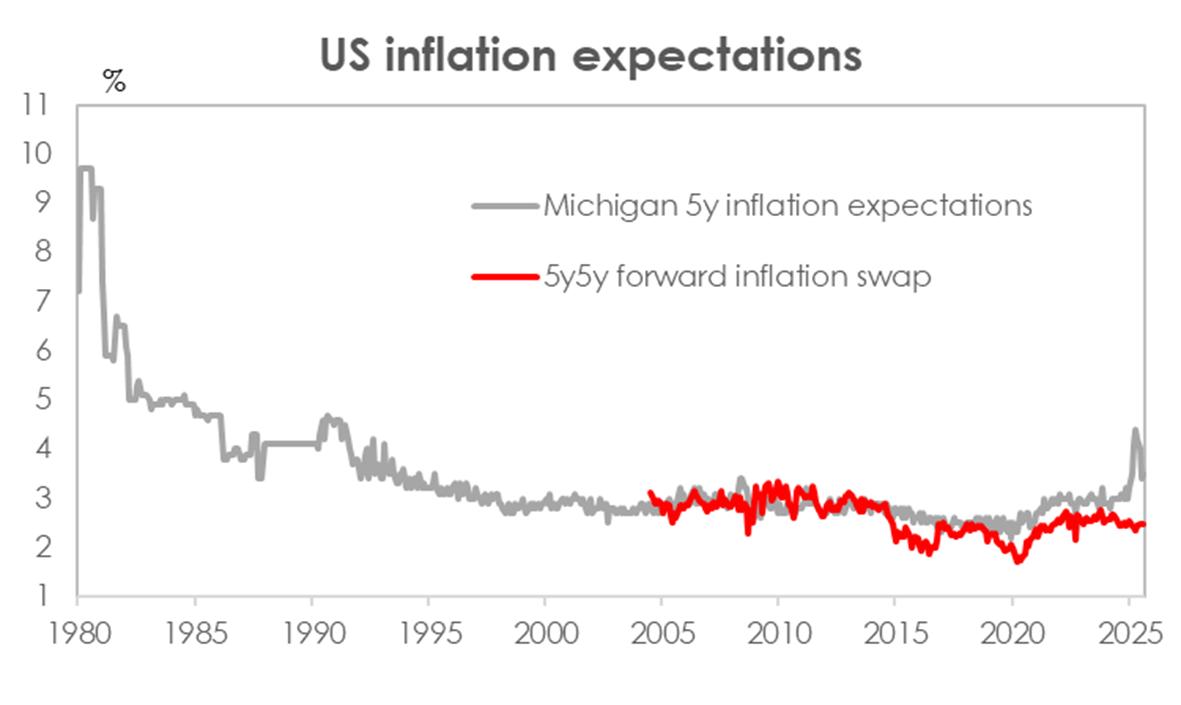

Concerns over the politicisation of the Fed are present in asset prices but remain muted. A loss of central bank independence would undermine the Fed’s credibility and increase the risk of higher inflation in the medium term. However, as the chart below shows, surprisingly little of the inflation risk is priced in for now. Investors still seem hopeful that the Fed will stay committed to keeping inflation stable and close to the 2% target. It is possible that the market believes President Trump will let the Fed get on with doing its job of supporting the goals of maximum employment and stable prices, despite his increasing influence over the Fed.

Inflation expectations remain anchored, but a loss of Fed independence would risk a de-anchoring

Source: University of Michigan, Bloomberg, Bank of Singapore

Or maybe, investors believe that the legal hurdles to political interference of the Fed are high. The betting market’s probability of President Trump removing Fed governor Lisa Cook fell back to around 30% after a brief spike in late August. However, if Trump succeeds in removing Cook or if the Fed cuts interest rates despite economic data suggesting otherwise, concerns about the Fed's independence could escalate. This could push gold prices well above USD4,000/oz.

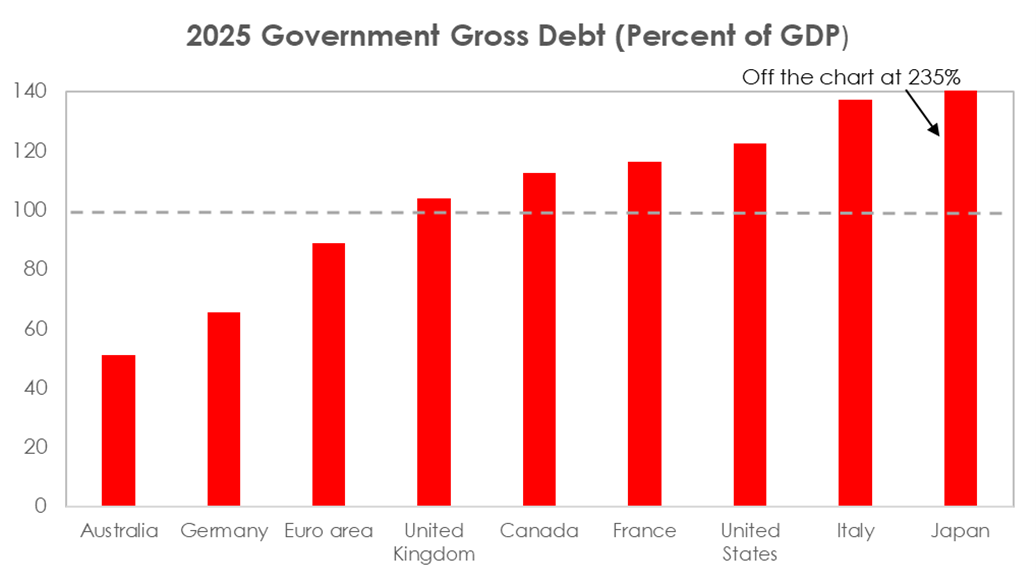

Much of the G10 world – the US, Canada, Japan and many of the bigger European economies apart from Germany – has big fiscal deficits and public debt above 100% of GDP. Unless there is greater political will to raise taxes or cut spending, central banks could come under increasing political pressure to inflate the debt problem away. “Fiscal dominance” – a scenario where central bank actions are not guided by an effort to achieve low inflation and full employment, but by the desire to avoid hard choices on taxes and spending – is a risk that investors increasingly need to weigh. High levels of debt can potentially erode the value and trust in fiat currencies. Investors will likely continue to build allocations to gold amid higher risk of savings in fiat currencies.

Debt over 100% of GDP and big deficits in most of the G10 world erode trust in fiat money

Source: IMF projections for 2025 from IMF Fiscal Monitor, Bank of Singapore

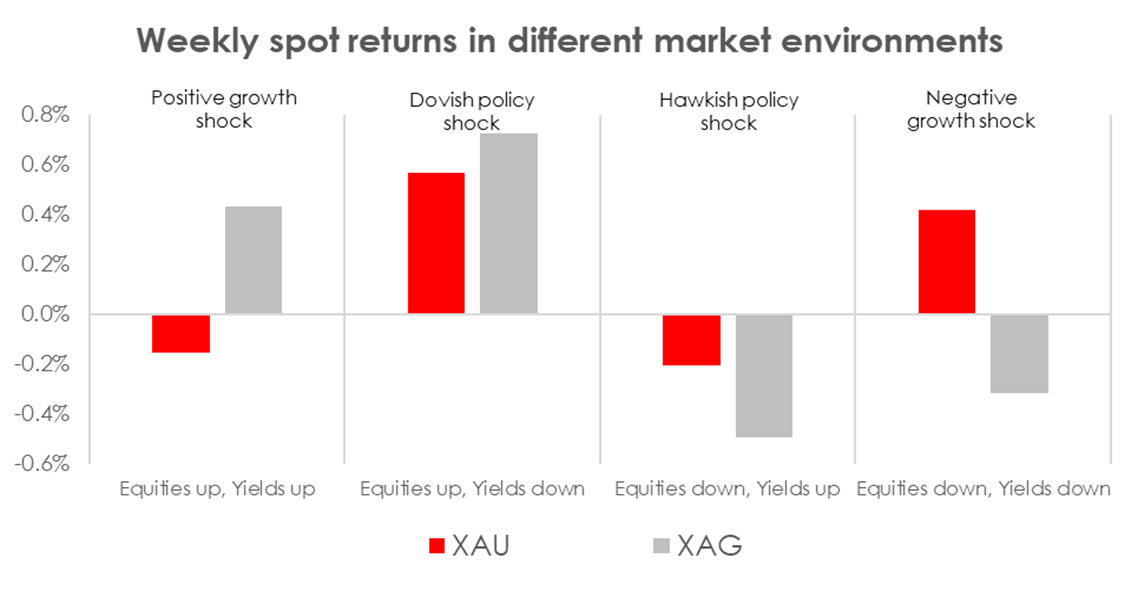

Silver has recently outperformed driven by hopes of a soft landing. However, gold could outshine silver if the global risk backdrop sours on stagflation fears. Our forecast favours gold over silver. Unlike gold, silver has numerous industrial uses and tends to do better in a rising equities environment, which usually corresponds to positive growth surprises or dovish policy shifts. Conversely, silver typically underperforms gold when the risk backdrop sours, especially when markets start to price in higher recession probabilities with lower yields and lower equities.

Silver typically underperforms gold when the risk backdrop sours

Note: We look at weekly returns from 2000-present. Equities refer to S&P 500 and Yields refer to US Treasury yields

Source: Bloomberg, Bank of Singapore

Important information

This product may only be offered: (i) in Hong Kong, to qualified Private Banking Customers and Professional Investors (as defined under the Securities and Futures Ordinance); and (ii) in Singapore, to Accredited Investors (as defined under the Securities and Futures Act) and (iii) in the Dubai International Financial Center to Professional Clients (as defined under the Dubai Financial Services Authority rules) only. No other person should act on the contents of this document.This product may involve derivatives. Do NOT invest in it unless you fully understand and are willing to assume the risks associated with it. If you have any doubt, you should seek independent professional financial, tax and/or legal advice as you deem necessary.

Please carefully read and make sure that you understand all Risk Disclosures, Selling Restrictions, and Disclaimers. This document must be read together with the relevant Prospectus & Offering Documents &/or Key Fact Statement.

Disclaimer

The Bank, its Affiliates and their respective employees are not in the business of providing, and do not provide, tax, accounting or legal advice to any clients. The material contained herein is prepared for informational purposes and is not intended or written to be used, and cannot be used or relied upon for tax, accounting or legal advice. Any such client is responsible for consulting his/her own independent advisor as to the tax, accounting and legal consequences associated with his/her investments/transactions based on the client’s particular circumstances.

This document and other related documents have not been reviewed by, registered or lodged as a prospectus, information memorandum or profile statement with the Monetary Authority of Singapore nor any regulator in Hong Kong or elsewhere.

This document may not be published, circulated, reproduced or distributed in whole or in part to any other person without the Bank’s prior written consent. This document is not intended for distribution to, publication or use by any person in any jurisdiction outside Singapore, Hong Kong, or such other jurisdiction as the Bank may determine in its absolute discretion, where such distribution, publication or use would be contrary to applicable law or would subject the Bank and its related corporations, connected persons, associated persons and/or affiliates (collectively, “Affiliates”) to any registration, licensing or other requirements within such jurisdiction.