Source: AFP.

Impact on credit markets so far

Since the start of the month with the US/Israel joint military action against Iran, volatility across risk assets has increased. Thus far, we have observed general unwinding of pre-war crowded trades as well as relative underperformance of long duration bonds month-to-date (MTD).

Credit markets were impacted by wider spreads from pre-conflict levels and higher US Treasury (UST) rates, with all segments posting negative total returns in the first week of March 2026. However, volatility in credit markets was relatively manageable compared to other asset classes.

We saw a bear flattening of the UST curve in the first week of March, as markets reduced its expectations of Federal Reserve (Fed) cuts in anticipation of potentially higher inflation as reflected in the 2Y UST breakeven yields.

How did credit spreads react to past episodes?

The financial market’s reactions to geopolitical events depends on prevailing valuations, economic cycle as well as the broader macro and financial environment. Thus, the impact of geopolitical events varies from episode to episode. However, there are still insights we can gain, looking back at historical geopolitical events to assess how credit spreads could react.

There have been instances where geopolitics have driven spreads materially wider such as during the Gulf War in 1990 and the Russia-Ukraine war in 2022; both being periods of a sustained rise in energy prices. Referencing the 2022 Russia-Ukraine War, an initial 50-70bps increase in IG spreads and 180-240bps increase in HY spreads were observed at the onset, before spreads gradually compressed when the situation stabilised.

However, in more recent events, such as the October 2023 Hamas attacks on Israel and Israel-Iran conflicts in June 2025, the impact on spreads from short spike in oil prices was more short-lived.

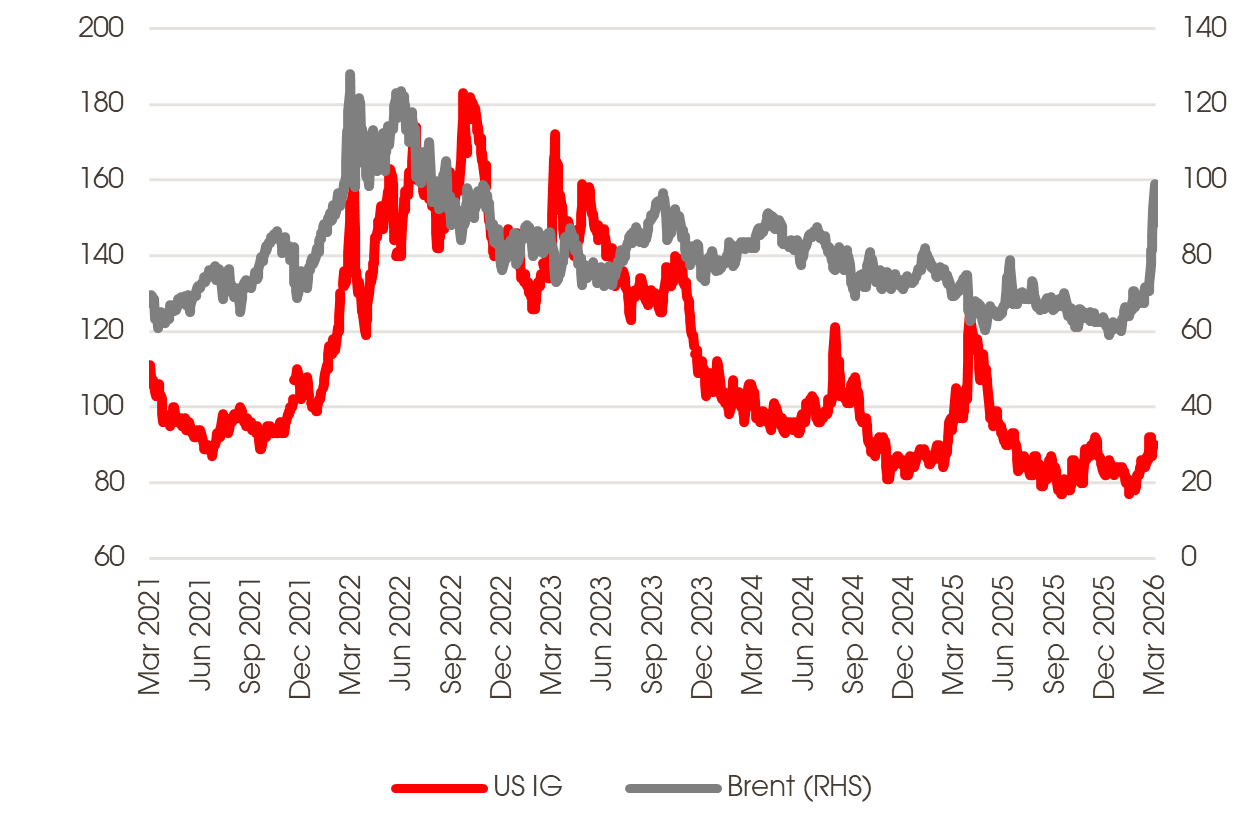

Exhibit 1: Past 5 years US IG Corporate spreads

Source: Bloomberg as of 9 March 2026

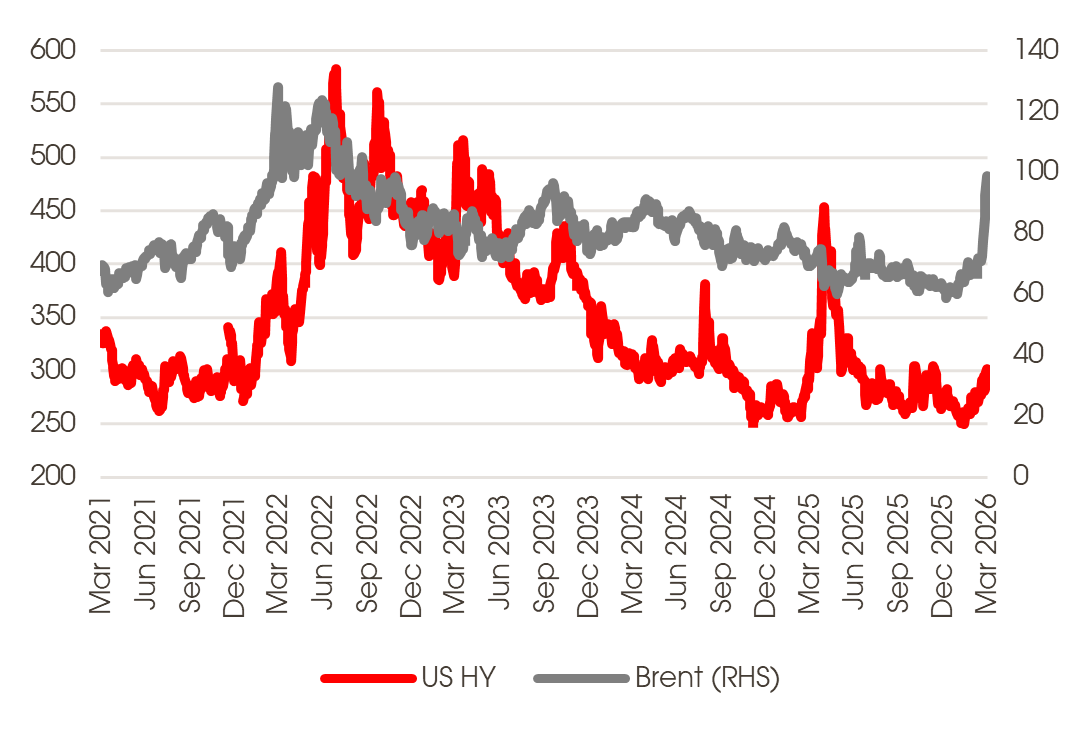

Exhibit 2: Past 5 years US HY Corporate spreads

Source: Bloomberg as of 9 March 2026

Sectoral and regional preferences in response to geopolitical events

In general, we expect cyclical sectors – such as ports, real estate, shipping, airlines, autos and consumer discretionary – as well as credits with weaker fundamentals and a heavier reliance on external financing to see larger spread widening on higher geopolitical risk premiums.

In contrast, defensive sectors such as telecom and consumer staples should be relatively better supported. As for utilities, it depends on how quickly the higher fuel cost can be passed through to end users, as certain countries may have price controls to ease the inflationary impact to the broader economy.

Earnings of energy producers should theoretically benefit from higher oil prices. However, the benefits from higher oil and gas prices are unlikely to be even across the energy sector, depending on the company’s operating and supply exposures to the disrupted region, the parts of the value chain it is involved and/or specifics around offtake contracts. For example, while upstream producers should directly benefit from higher oil prices, the extent to which benefits accrue depend on the proportion of output sold at fixed contract prices or spot prices. Another important consideration is whether the producer has a reasonably high proportion of operating assets in the affected region which could cause operating disruption.

While the earnings of energy producers could potentially be supported by higher prices, unlike equities, energy bonds may not be a good geopolitical hedge if there is a positive correlation between rates and oil price.

At the other end of the spectrum, we think energy importers, downstream refiners and petrochemicals companies could face higher feedstock/input cost and/or supply disruptions if it relies on supplies from Middle East. The final net impact will depend on whether they can and how long it takes to pass-through higher costs to end users.

Most IG Oil & Gas (O&G) issuers in EM under our coverage are quasi-sovereigns, and we expect spread changes in these issuers to largely track movements in their respective sovereign credits, owing to the strategic importance to their sovereigns. Although the GCC region did benefit in 2022 from higher oil prices, given the risks to logistics this time the benefits may not similarly accrue to GCC producers, in addition to the added geopolitical premium.

Region wise, we will expect Middle East to be more negatively impacted, followed by Asia and Central & Eastern Europe, while Latam and Africa should be more resilient due to their commodity exposures.

However, the impact on specific bonds prices will also depend on its earnings and business profiles, rates movements, overall market sentiment and technicals. For example, while Asia credits could be indirectly impacted by higher energy prices and near-term volatility, market technicals could provide some downside support to bond prices. Within Asia, we expect high quality China IG names to hold up better than higher beta India/Indonesia/Thailand issuers given the technical support and potential rotation from GCC credits back to home base for domestic investors.

Portfolio implications

Although President Trump commented that the war “could be over soon” and is reportedly mulling possible options to combat surging oil and gas prices – among which was tapping on the G7 countries’ strategic oil reserves if necessary – there were few details. Iran’s response to the headlines will be important.

We believe the key to energy price normalisation would be re-opening of the Strait of Hormuz and resumption of suspended oil and gas production. The geopolitical situation remains fluid, and we will continue to stay prudent till more clarity emerges on length of war and central banks’ response. Oil price futures remained above the level pre-strikes. For spreads to decompress materially, there needs to be a sustained spike in oil prices.

We believe the ultimate impact on credit fundamentals and spread reaction will depend on the scale and duration of the conflicts. Recent increases in rates volatility alongside higher oil prices is likely to add to the complexity of credit markets, widening risk premium and spread volatility.

Important information

This product may only be offered: (i) in Hong Kong, to qualified Private Banking Customers and Professional Investors (as defined under the Securities and Futures Ordinance); and (ii) in Singapore, to Accredited Investors (as defined under the Securities and Futures Act) and (iii) in the Dubai International Financial Center to Professional Clients (as defined under the Dubai Financial Services Authority rules) only. No other person should act on the contents of this document.This product may involve derivatives. Do NOT invest in it unless you fully understand and are willing to assume the risks associated with it. If you have any doubt, you should seek independent professional financial, tax and/or legal advice as you deem necessary.

Please carefully read and make sure that you understand all Risk Disclosures, Selling Restrictions, and Disclaimers. This document must be read together with the relevant Prospectus & Offering Documents &/or Key Fact Statement.

Disclaimer

The Bank, its Affiliates and their respective employees are not in the business of providing, and do not provide, tax, accounting or legal advice to any clients. The material contained herein is prepared for informational purposes and is not intended or written to be used, and cannot be used or relied upon for tax, accounting or legal advice. Any such client is responsible for consulting his/her own independent advisor as to the tax, accounting and legal consequences associated with his/her investments/transactions based on the client’s particular circumstances.

This document and other related documents have not been reviewed by, registered or lodged as a prospectus, information memorandum or profile statement with the Monetary Authority of Singapore nor any regulator in Hong Kong or elsewhere.

This document may not be published, circulated, reproduced or distributed in whole or in part to any other person without the Bank’s prior written consent. This document is not intended for distribution to, publication or use by any person in any jurisdiction outside Singapore, Hong Kong, or such other jurisdiction as the Bank may determine in its absolute discretion, where such distribution, publication or use would be contrary to applicable law or would subject the Bank and its related corporations, connected persons, associated persons and/or affiliates (collectively, “Affiliates”) to any registration, licensing or other requirements within such jurisdiction.