Source: AFP.

A landslide victory for Takaichi and the LDP

On 8 February 2026, Japan held a snap general election called by Prime Minister Takaichi, leader of the ruling LDP, which won a historic landslide securing 316 of 465 seats − the largest post-war victory for any single party.

LDP’s supermajority hands a strong mandate to Takaichi, whose party can now override vetoes from the Upper House and initiate constitutional amendments.

Market reaction reflects a mix of optimism and caution

Financial markets reacted swiftly to Takaichi’s decisive win, reflecting both optimism about political clarity and concern about Japan’s fiscal trajectory.

On one hand, Japanese equities surged sharply after the result, with the Nikkei 225 Index hitting record highs immediately following the vote as investors priced in expansionary fiscal policy and stronger growth prospects.

On the other hand, JGBs sold off; which resulted in yields rising across the curve − with two-year yields reaching multi-decade highs − on expectations of increased issuance to fund fiscal stimulus and consumption tax relief, reflecting investor unease about financing large fiscal measures against Japan’s already heavy sovereign debt load.

Finally, the JPY’s reaction has been mixed since the election result. Initially, the currency weakened − consistent with the “Takaichi trade”: long equities, short bonds, short yen − in anticipation of aggressive fiscal expansion and prolonged loose monetary conditions. However, the JPY later stabilised and strengthened slightly as authorities signalled vigilance on volatility and potential intervention measures.

Overall, although equities have rallied on clarity of policy and fiscal promise, the fixed income and FX markets have remained tentative, underscoring the balancing act between growth optimism and fiscal realism.

Takaichi’s economic platform arguably comprises the “second and third arrows” of Abenomics. Rather than broad-based stimulus, the focus of her fiscal policy is targeted at “crisis management investment” in specific sectors such as defence, energy security, cybersecurity, and disaster resilience.

Importantly, Takaichi has emphasised the concept of “responsible and proactive fiscal policy”, which prioritises economic growth over immediate fiscal consolidation.

While the “responsible” label plays an important role in placating bond markets, Takaichi has argued that fiscal sustainability is impossible without growth, which underscores her significant spending commitments, such as the abolition of provisional gasoline taxes and the lifting of marginal tax thresholds to support household disposable income.

Japanese equities tend to respond positively to single party majority victories

Historically, the Japanese equity market tends to respond positively to a single party majority win. The fact that the Takaichi administration is expected to govern with a relatively high degree of stability and be able to pursue changes and pro-cyclical fiscal priorities is likely to be a supportive factor. That said, the risks of currency and bond yield volatility, if excessive, could negatively impact the equity market and should be carefully watched.

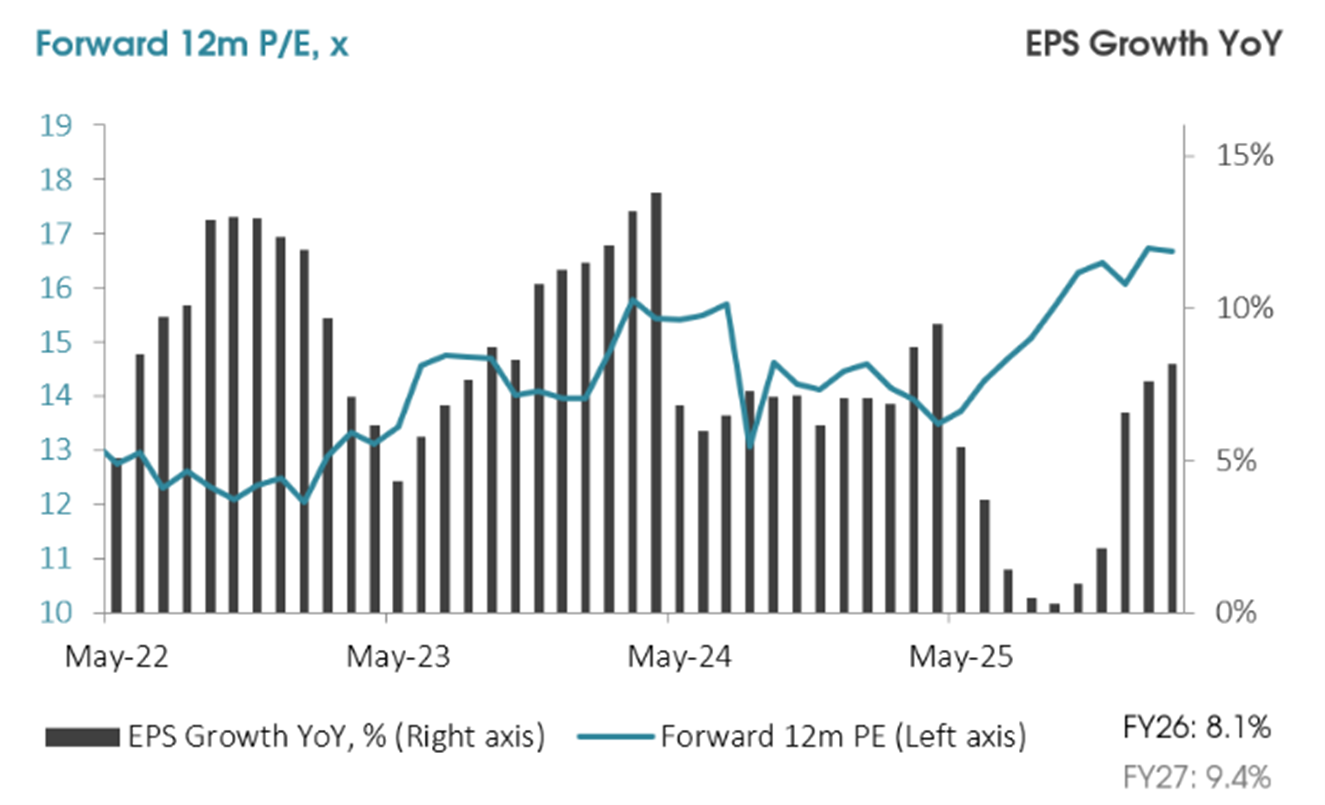

Exhibit 1: MSCI Japan EPS growth and forward 12m P/E

Note: For Japan, FY stands for fiscal year (accounting year), which is a twelve-month period starting in April in Japan. FY26 = Fiscal year ending March 2026, FY27 = Fiscal year ending March 2027

Source: I/B/E/S Refinitiv Datastream, Bank of Singapore; data as of 9 Feb 2026

We continue to hold a neutral position in Japanese equities. Looking ahead, we believe investors will continue to shift their focus towards a "Sanaenomics" portfolio weighted toward high-beta exporters, defence, and strategic industrial sectors.

In particular, Takaichi’s administration has highlighted 17 strategic sectors, including AI, semiconductors, and shipbuilding, which are viewed as essential for national security. This approach creates a “security premium” for stocks in these industries, shifting the focus from general cyclical growth to state-directed industrial policy.

Cautious of JGB volatility risks

JGBs yields could continue to face upward pressure given Takaichi's proposal for a two-year suspension of consumption tax on food items, which has created concerns over funding and set off JGB volatility.

The 10Y JGB yield has risen significantly since Takaichi took office due to a rising term premium driven by funding concerns and Takaichi's shift from a single-year primary balance target to a multi-year “stock-based” assessment.

JPY likely to be rangebound over near-term

Takaichi’s stance on the Bank of Japan (BoJ) has been a primary driver of JPY weakness, characterised by her preference for a “high-pressure economy” that runs hot to generate demand-pull inflation. That said, Takaichi has moderated her tone since calling rate hikes “stupid” in 2024, and her administration now tacitly accepts interest rate normalisation only if it does not derail growth, which suggests that the JPY is likely to range between 150-160 over the near term.

Important information

This product may only be offered: (i) in Hong Kong, to qualified Private Banking Customers and Professional Investors (as defined under the Securities and Futures Ordinance); and (ii) in Singapore, to Accredited Investors (as defined under the Securities and Futures Act) and (iii) in the Dubai International Financial Center to Professional Clients (as defined under the Dubai Financial Services Authority rules) only. No other person should act on the contents of this document.This product may involve derivatives. Do NOT invest in it unless you fully understand and are willing to assume the risks associated with it. If you have any doubt, you should seek independent professional financial, tax and/or legal advice as you deem necessary.

Please carefully read and make sure that you understand all Risk Disclosures, Selling Restrictions, and Disclaimers. This document must be read together with the relevant Prospectus & Offering Documents &/or Key Fact Statement.

Disclaimer

The Bank, its Affiliates and their respective employees are not in the business of providing, and do not provide, tax, accounting or legal advice to any clients. The material contained herein is prepared for informational purposes and is not intended or written to be used, and cannot be used or relied upon for tax, accounting or legal advice. Any such client is responsible for consulting his/her own independent advisor as to the tax, accounting and legal consequences associated with his/her investments/transactions based on the client’s particular circumstances.

This document and other related documents have not been reviewed by, registered or lodged as a prospectus, information memorandum or profile statement with the Monetary Authority of Singapore nor any regulator in Hong Kong or elsewhere.

This document may not be published, circulated, reproduced or distributed in whole or in part to any other person without the Bank’s prior written consent. This document is not intended for distribution to, publication or use by any person in any jurisdiction outside Singapore, Hong Kong, or such other jurisdiction as the Bank may determine in its absolute discretion, where such distribution, publication or use would be contrary to applicable law or would subject the Bank and its related corporations, connected persons, associated persons and/or affiliates (collectively, “Affiliates”) to any registration, licensing or other requirements within such jurisdiction.